Gold prices posted another weekly decline at the close on Friday and they finished the session at $1,584 per ounce. Albeit the net weekly erosion in value was on the order of only two-thirds of a percent, the overriding sentiment among participants was still indicative of significant disappointment about the Fed not handing out a fresh batch of "easy money" as well as of a lack of a perceived safe-haven premium that the yellow metal ought to carry instead of behaving like a risk asset.

Gold prices posted another weekly decline at the close on Friday and they finished the session at $1,584 per ounce. Albeit the net weekly erosion in value was on the order of only two-thirds of a percent, the overriding sentiment among participants was still indicative of significant disappointment about the Fed not handing out a fresh batch of "easy money" as well as of a lack of a perceived safe-haven premium that the yellow metal ought to carry instead of behaving like a risk asset.

The new trading week was off to a rocky start in precious metals as, despite only a relatively small, 0.20% advance in US dollar (to just above 83.80 on the index) the complex headed for lower price ground overnight and at the opening bell in New York.

Spot gold touched lows at under the $1,563 level losing $22 in pre-market action, while spot silver reached $26.75 per ounce and fell about 60 cents. The latest Standard Bank (SA) analysis and market positioning report highlights a "decidedly bearish" outlook in the silver futures market. Total short positions in the white metal stand at nearly 103 million ounces and are now approaching their one-year record that stood at 109.6 million ounces.

Platinum dropped $23 to a quoted bid at $1,388 and palladium declined $9 to $565 the ounce. Rhodium was bid at $1,200 per troy ounce. The platinum-group metals’ sector is experiencing some major pain in the wake of falling prices and the fact that the South African noble metals’ output has fallen some 25% through the end of May as compared to one year ago is not yet helping values amid this risk-off maelstrom. Shares of certain miners have fallen dramatically; among the worst hit are Aquarius (down almost 84%) and Eastern Platinum (down more than 75%). Aquarius has actually halted the majority of its production at this juncture. Amplats had something to say about the situations as well.

In other markets crude oil fell 1.31% and copper… topped base metal declines with a loss of 2.56%. The euro flirted with the $1.20 pivot level as the eurozone crisis flared up once again in the wake of soaring Spanish bond yields and the IMF’s cutting off of Greek aid. Italian equity markets suffered a 5% shellacking today as investors ran for the crowded exit doors. Dow futures appeared to portend an unpleasant day in the making in New York.

The UK’s Telegraph notes that

"almost all of this year’s gains have been wiped out, with the gold price now just 1%. above its end-2011 level."

The Kitco Charts and Data page shows that gold started 2012 at $1,598 per ounce and that it is thus down 1% from that level as of this writing. The Telegraph remarks that

"[The] gold bugs are banking on QE3, a further round of quantitative easing from the Federal Reserve, to get the price moving again. But as the year progresses it’s nowhere in sight."

Meanwhile, Commerzbank analysts pointed to the continuing gold ETF outflows as evidence that the precious metal is "currently in lower demand." Nice euphemism.

Speaking of demand, specifically that on the physical side of the gold equation, the Reserve Bank of India’s Deputy Governor, Dr. K.C. Chakrabarty, sounded a bit like… Warren Buffett over the weekend when he addressed the issue of his institution’s attempts to curb Indian gold demand for the sake of righting the difficult current account deficit that his country faces. Dr. Chakrabarty remarked that

"there is no intrinsic value in the speculative investment of gold" and that "the precious metal can’t be used for anything productive, [that it] gains in value only because of a “mad rush” for the commodity among speculators, and the day [that] this will end, the price will fall sharply."

Dr. Chakrabarty also noted in Mumbai this weekend that in order to achieve the aims of India’s central bank as regards the dampening of domestic gold demand, nothing short of a "big shift in people’s social and cultural attitudes towards gold" would do the job, highlighting the fact that

"the societal obsession with gold is an archaic idea of the pre-historic times when India was a rich society of abundance."

The problems that India is currently grappling with within the context of its burgeoning current account deficit have been attributed almost entirely to the large amounts of gold and oil that the country imports on an annual basis.

However, the Deputy Governor had more than just the unbalanced Indian fiscal situation in mind when he advised that India’s gold "problem" has become quite estranged from what one might call the traditional so-called "love" trade and that the appetite for gold has, by now, unfortunately morphed into the "love of quick money" trade. Dr. Chakrabarty warned that investments in gold by India’s poor denizens are "troublesome" and that the RBI has already been attempting to thwart the mushrooming of gold-based loans and gold coin sales activities at the nation’s banks.

He said that "The problem is that it [gold investing] has become a culture where the poor people are purchasing and ultimately, they are borrowing on that gold at 30 per cent [interest]."

The RBI therefore sees the aggravation of the nation’s current account deficit as an unnecessary side-effect of the appetite for gold. This kind of "love trade"- if carried into the extreme- could turn into the "hate" trade, at least as far as India’s government is concerned.

Incidentally, India just elected its 13th President, Mr. Pranab Mukherjee yesterday. His election might be a "signal" to the RBI to keep up its efforts aimed at suppressing the nation’s appetite for the yellow metal. Mr. Mukherjee, you might recall, in his role as India’s Finance Minister, was quite recently very adamant about the maintenance of a newly instituted customs duty hike on gold, and he saw it as more than justifiable.

Most of the country’s jewellers and vendors went on a nationwide strike in March to protest the tariff increases on bullion. Mr. Mukherjee warned back then that

"the import of gold of such magnitude [circa 900 annual tonnes] strains [India’s] balance of payments and affects exchange rate of rupee through impacting [the] supply-demand balance of foreign exchange."

This is a story we would advise following closely as it develops further. The gold market cannot, and will not, ignore what might result from regulatory changes or other restrictive measures in a country that normally consumes the kind of gold tonnage that it normally does.

Even if illicit smuggling were to flourish in India, as many predict, the net lost tonnage demand would yield a gold market under even more pressure to absorb surpluses via investment offtake. One cannot yet estimate what the loss of, say, 450 tonnes of physical Indian demand would do to world gold prices, but, at the moment, the gold market requires more than $120 billion in constant annual investment demand to remain "afloat." This means that nearly 2,400 tonnes of gold need to be mopped up by investment demand each year, and on an on-going basis to just maintain prices near current levels. As noted here recently, the net additions to investor gold holdings declined by nearly 6% in 2011 and they added up to only 1,067 tonnes. To be continued…

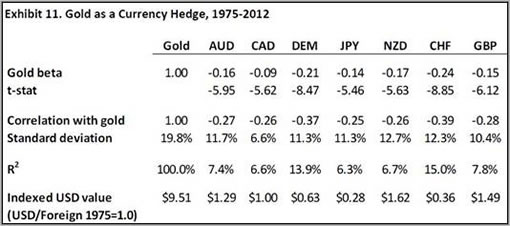

While we are on the subject of continuing installments, we now bring you a couple more insights from the recently published and discussed academic research paper by commodities expert Claude Erb and Duke University Prof. Campbell Harvey. In last week’s article we covered the topic of gold and inflation-hedging but did not exactly come to an encouraging conclusion. Today, we will take a look at gold as a hedge against currencies. We will cover gold as a putative safe-haven and other similar beliefs in upcoming articles. Myth-busting never take a break here.

The Erb/Harvey study starts with the commonly held truism that "gold is a currency hedge." In other words, note the authors, if the US dollar loses 10% against the yen, for example, then the price of gold should offset that loss by rising an equivalent 10%. That argument, unfortunately, only holds water if in fact one of the two countries involved in such a calculation/hedging can consistently boast of an inflation rate of… zero percent.

What has, in fact, taken place is that, since 1975, the US dollar price of gold has risen and the US dollar has depreciated against the yen. On the other hand, the price of gold in yen also rose and the Japanese yen appreciated against the dollar. Last week, the World Gold Council (EGC) issued its report on the gold price performance in the second quarter of 2012, in which it noted that gold prices declined in most currencies with the exception of the euro, the Swiss franc and the Indian rupee.

For any particular currency pair, if gold is able to hedge one country’s currency, it certainly is not able to hedge the other’s currency. As regards gold as a hedge against "domestic" (pick your country) currency "debasement" (courtesy of the imaginary printing presses that are putatively running 24/7) the authors find that, from a macro-perspective, the mantra of "currency down –gold up" also does not hold true. As regards the following table of currencies, the authors conclude, there seems to be little connection between currency returns and gold returns:

All (speculative) eyes are now focusing on Friday’s US Q2 GDP report. You already know how that news day will play out; feeble growth figures will stoke the commodity bulls who will immediately read an imminent QE3 into the statistical "coffee grounds" on offer from the US Commerce Department. The US economy grew at the 1.9% rate in Q1 and estimates are that such expansion may have stalled to near 1.3% during the most recent quarter. Separately, a Chinese central bank advisor has warned this weekend that his country’s economic expansion could slow to 7.4% in the current quarter and that the contractive phase is not yet over. Much hangs in the balance these days. IMF Chief Ms. Lagarde has warned that this crisis knows no borders and that it is knocking on everyone’s doors.

Until Wednesday, well, hang in there…

Senior Metals Analyst — Kitco Metals

Jon Nadler

Senior Metal Analyst

Kitco Metals Inc.

North America

Disclaimer: The views expressed in this article are those of the author and may not reflect those of Kitco Metals Inc. The author has made every effort to ensure accuracy of information provided; however, neither Kitco Metals Inc. nor the author can guarantee such accuracy. This article is strictly for informational purposes only. It is not a solicitation to make any exchange in precious metal products, commodities, securities or other financial instruments. Kitco Metals Inc. and the author of this article do not accept culpability for losses and/ or damages arising from the use of this publication.

www.kitco.com and www.kitco.cn

Blog: http://www.kitco.com/ind/index.html#nadler