Precious metals (as well as other commodity and some equity) markets settled lower on Thursday as the pressure exerted by a very robust US dollar took its toll and speculators turned risk-averse once again.

Precious metals (as well as other commodity and some equity) markets settled lower on Thursday as the pressure exerted by a very robust US dollar took its toll and speculators turned risk-averse once again.

Spot gold ended with a loss of $13 at $1,603 per ounce in New York after some bulls exhibited apprehensions about easing prospects by the Fed ebbing owing to better job creation numbers from ADP.

Silver shed 2.1% to finish at $27.70 the ounce. So far as gold prices do not manage to vault above the $1,633-$1,640 resistance area the prospects of a quick jaunt to $1,700 remains a bit remote. On the other hand, it would still take the demolition of the $1,525 support zone in the yellow metal to embolden the bears in a major way. Silver is stuck within similar confines and its numbers to watch are $26.10 on the low end and $29.10 on the upper one.

Platinum dropped $16 after a major advance on Tuesday and ended at $1,469 per ounce, while palladium lost $15 to close at $583 the ounce. Very good US car sales figures reported earlier in the week were unable to lend support yesterday as overcoming the greenback’s advance was a tall order in commodities in general. Adding to the downbeat tone was the background realization that perhaps all of the current central bank easing mania is actually a reflection of rekindled deflationary pressures and anxieties surrounding a spreading recession. Crude oil finished about 1% lower at $86.82 per barrel while the Dow retreated by 47 points on the session.

In yet another classic example of "buy the rumour, sell the fact" gold prices fell to under the pivotal $1,600 level in early Thursday trading action despite accommodative gestures from the Chinese, British, and European central banks. At the end of the day, the largely anticipated easing moves by the aforementioned monetary authorities ended up benefiting the US dollar — it surged more than two-thirds of a percent to reach 82.81 on the trade-weighted index.

Up to the time of the actual morning announcements by the aforementioned trio of central banks, gold and other commodity specs had aggressively tried to lift prices under the cover of the excuse that such strategy is a) good for more risk-taking and b) that it will yield strong inflation within a few months and c) that it is detrimental to the dollar. Oops. Not so fast. As the Financial Times put it yesterday, global investors chose to listen to what central bankers said (overtly as well as between the lines) as opposed to focusing on the easier money they offered.

There is a school of thought that interprets China’s second rate cut in one month as a precursor to some really feeble economic stats to soon be released. The country’s economic growth may have skidded for a sixth quarter as the troubles in the Old World took their toll on exports and as the "adjustment" phase of the domestic real estate bubble rolls on. The best hope now is to try to get things to produce a 7.5% GDP reading on the 13th of the month. That same school of thought translates the ECB’s rate cut move as important only insofar as it is an attempt to try to get banks to lend some money in order to get things finally moving into the right direction in Europe.

With regional unemployment above 11% as of the latest reading, that would indeed by a worthwhile priority. The problem, as Bloomberg News sees it is that

"however innovative the drive toward zero rates is, the ECB is not stepping outside the role it has played for the past few years and the levers it’s pulling on offer very little play. Without a broader mandate the ECB’s ability to contribute to the resolution of the credit crisis is likely to wane.

Indeed, just one week after the "watershed" 19th EU summit, the markets have very little to bite into insofar as an enhanced ECB, or a visibly sounder footing for Spain, for example. Its cost to borrow ten-year funds climbed to the highest level in seven months yesterday.

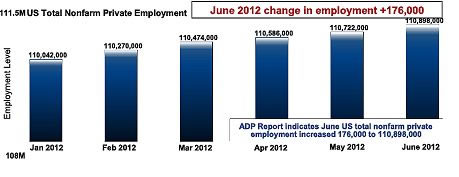

The combination of the euro’s decline to under $1.24 after the ECB cut its key rate to a new historic low of 0.75% (and its deposit rate to nil!) and the better-than-expected ADP private sector employment report clearly played into the hands of dollar-longs and it unwound much of the gain that had been posted on Tuesday in the precious metals’ complex.

The latest unemployment claims filings also added to the greenback’s Thursday rally; they fell by 14,000 (a two-month high) to six-week lows at 374,000. More importantly, the June 2012 ADP National Employment Report found that 176,000 jobs were created in June and that figure was 76,000 better than economists had forecast. Don’t know about you, but we kinda/sorta see a… trend in the ADP-sourced image below?

It now appears that Turkey may have found a solution to the problem that has been vexing Indian governmental authorities; what to do about the gold under the nation’s mattresses, the [previously] soaring gold imports, and the nation’s current account deficit. Evidently, even though the strategy does have a ‘cost’ it is as simple as letting folks open digital gold savings accounts. Basically, a gold deposit account permits an owner to make withdrawals in either little bullion ingots or in Turkish lira amounts.

Interest rates on such accounts are significantly lower than comparable ‘normal’ time deposits. The scheme is diverting (some say to a seriously damaging extent) the flow of gold into Turkish bazaars and jewellery shops. However, it does seem to play into the hands of the government’s aims to free up the sizeable amount of "mattress gold" around the country and to reduce gold imports and, along with those, the current account deficit. Hard core gold bugs, of course, would be loath to ever hand over their "stack" to a bank in return for a claim to the holdings. Meanwhile, India continues to seek other ways in which to curb domestic gold appetites. Up through mid-year its efforts appear to have "paid off" when judged by the 58.7% slump in H1 2012 gold imports (down to 250 tonnes on the period).

The lack of same has resulted in the closure of more than 500 gold-selling shops in Saudi Arabia earlier this year. The blame was directed at the recent climb in gold prices and the statistics that have accompanied the closures ought to be raising more than just some eyebrows over at the World Gold Council (which is funded by the world’s gold producers who are apparently mesmerized by how much gold they have been able to move –up to a point- by the creation of gold-based ETFs). To wit: Saudi gold sales fell by 50% and sales are seen as declining further for the remainder of 2012. Traditionally strong sales periods during the Haj and Umrah periods have not managed to offset the falling gold offtake in the nation.

Troubles of a different ilk continue to afflict miner Newmont and its Peruvian operation Minas Congas. A state of emergency had to be declared by Peru’s government after five deaths related to the on-going protests against the company owing to the potential environmental impact of the aforementioned operation. Newmont has already sunk in $800 million of an eventual $4.8 billion into the Minas Congas project while Peru is looking at planned mining firm investments of over $50 billion over the next decade as being at risk from the rising unrest among its citizens.

Peru is thought to contain huge mineral resources and it is already the world’s second-largest copper and sixth largest gold producer. It is thus understandable how four-digit gold prices have engendered "gold fever" among foreign mining firms wanting to dig up its soil and among local politicians eager to reap the benefits of huge inflows of investment. This "gold fever" on the other hand, given the rising "temperatures" among the citizenry which feels economically left out and/or at risk of being polluted to death might well claim the leadership of President Ollanta Humala.

The mining industry’s situation is no less muddled over in South Africa this week. A conference of the African National Congress has failed to come up with any concrete pronouncement of the thorny subject of mine nationalization. To be sure, the idea of a mass, all-encompassing nationalization appears to have been struck from the ANC agenda but that does not mean that partial nationalization and the creation of a list of "strategic minerals" (read: ones we will never let go of and whose mines we will fully take over) remains very much on the "to-do" list. In terms of what might be done, well, we will have to wait until at least December and possibly until 2104’s general ANC elections to see some concrete results along this contentious front.

This morning’s trading action tilted to the downside once again as the pre-Labor Department jockeying for position appeared less concerned with the Labor Department’s report and more with dire warnings by the IMF’s Ms. Lagarde that the global economy’s growth estimate will have to be reduced in view of emergent weak patterns in the economies of… well, almost everyone’s.

Without giving specific numbers on the global GDP, Ms. Lagarde noted that the global economy is "tilted to the downside" and that estimates made 90 days ago are now in need of revision. The only bright spot seen by Ms. Lagarde is on the fiscal side of things, and in only one country: Japan. That nation is trying its utmost to slash its debt burden and is therefore about to pass legislation intended to double its sales tax rate to 10% by 2015. Try that one in the US of A, Messrs. Obama and/or Romney…

Spot gold fell to lows near $1,587 and then opened at $1,596, down $7 while silver touched $27.25 per ounce overnight but opened at $27.52. Once again, the US dollar added a few small steps to yesterday’s upward march and reached 82.85 on the index. Crude oil appeared to be ahead of the morning’s game with a solid negative tone of 2.1%. Consensus had the US non-farm payrolls data coming in at 100,000 for the month of June.

The view that "the [US] labor market is struggling but healing" was underscored with the release of the June jobs creation numbers this morning. American employers made room for 80,000 jobs last month, and while the figure was below estimates, it was a better one than that we saw in May (69,000). The national jobless rate remained at 8.2%.

The initial reaction in commodities was a… non-reaction. Gold attempted a rise and it managed a roughly $5 one but gave up after just 9 minutes after the report’s issuance and was once again down by nearly $10. The rest of the complex remained solidly mired in the red zone of price tickers as of this writing.

Silver, the PGM group, as well as copper and crude reflected the IMF concern while gold specs initially tried to glean some Fed "give" from the jobs report, but then realized that, alas, [for the bulls] this production by the US Labor Department will not go down in history as the one that "forced" the Fed’s hand. In fact, safe-haven flows were squarely aimed at the greenback in the aftermath of the jobs figures and the US currency came to within striking distance of the 83 mark on the index. Keep an eye on that buck, folks. It dictates the game this summer.

Have a nice weekend.

Jon Nadler

Senior Metals Analyst — Kitco Metals

Jon Nadler

Senior Metal Analyst

Kitco Metals Inc.

North America

Disclaimer: The views expressed in this article are those of the author and may not reflect those of Kitco Metals Inc. The author has made every effort to ensure accuracy of information provided; however, neither Kitco Metals Inc. nor the author can guarantee such accuracy. This article is strictly for informational purposes only. It is not a solicitation to make any exchange in precious metal products, commodities, securities or other financial instruments. Kitco Metals Inc. and the author of this article do not accept culpability for losses and/ or damages arising from the use of this publication.

www.kitco.com and www.kitco.cn

Blog: http://www.kitco.com/ind/index.html#nadler