Volatility and indecision patterns dominated Thursday’s trade in gold and silver while platinum and palladium posted solid gains on the session. The yellow metal darted back and forth from gains to losses and traded over a relatively wide, $20 range as market participants attempted to capitalize on the most recent increase in jobless claims, then on the hefty decline in US May consumer prices, and finally on the continuing flow of euro crisis-related news.

Volatility and indecision patterns dominated Thursday’s trade in gold and silver while platinum and palladium posted solid gains on the session. The yellow metal darted back and forth from gains to losses and traded over a relatively wide, $20 range as market participants attempted to capitalize on the most recent increase in jobless claims, then on the hefty decline in US May consumer prices, and finally on the continuing flow of euro crisis-related news.

The final session of this week opened in New York this morning with an equal lack of directional conviction in precious metals. Gold fell $3 to the $1,620 mark while silver was off by 6 pennies at $28.58 the ounce. Platinum was down $5 at $1,483 while palladium declined $2 to $629 per ounce. Background markets showed crude oil up 18 cents at $84.09 and the US dollar up 0.06 at 81.93 on the index. The euro managed to tread water just above the $1.26 level and stock index futures were pointing higher on central bank "pep" talk regarding their readiness to step in if events warrant on Monday.

Bullion is still confined to the $1,550-$1650 trading range and on the technical side of its paradigm there is nothing much new to report. Michael Shaoul, the New York-based chairman of Marketfield Asset Management said that gold prices may decline to as low a level as $1,300 later this year after they breach support at $1,520 per ounce. Mr. Shaoul remarked that gold is not a "viable alternative" to [fiat] currencies. Speaking at a Bloomberg Link conference in Boston on Thursday, Mr. Shaoul cautioned that monetary easing by various central banks will not "inevitably" lead to a moonshot in gold prices.

For the time being, with Sunday’s Greek elections and next week’s FOMC meeting still looming, few players were evidently willing to go beyond a few quick intra-day plays and they were mainly shadowing movements in the US dollar and the euro. Economic data is taking a back seat with speculators these days, unless it points to a potential scenario whereby the Fed might bestow additional free money on the markets.

In terms of no fresh bullish news, the situation is not a whole lot different on the retail physical investment scene. India’s Commerce Ministry reported a 52% decline in May’s gold and silver imports into the country. The Economic Times reports that gold-based ETFs have seen net outflow of Rs 41 crore [a crore is equal to ten million] in May, according to data reported by the Association of Mutual Funds in India. Meanwhile, Indian jewelers still report opportunity-driven gold sales by local consumers.

As noted, would-be gold buyers in India remain sidelined while sellers outnumber them as they all watch record prices in local terms persist. Then again, huge numbers of that country’s denizens are undergoing an existential struggle to simply feed themselves. At the same time, there has not been any notable increase in European offtake despite the reported 600 to 900 million euros’ worth of outflows from Greek bank deposits on a daily basis. The Swiss franc and the dollar appear to be drawing those safe-haven bids for the time being.

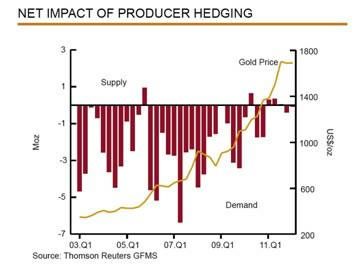

Thomson Reuters GFMS just released its QI global gold hedge book analysis and it contains a number of notable findings. First and foremost, is the fact that the global outstanding producer hedge book is now down to a paltry 158 tonnes. Second, GMFS believes that in 2012 we will once again be witnessing slight net hedging by producers. You recall that 2010 and 2011 saw the first emergent signs of hedging among miners. In fact, the bulk of the first quarter’s activity in this niche came from hedgers and there was little active de-hedging.

We once again bring this important paradigm shift to your attention owing to the fact that the extended period of time during which miners took metal from the market in the process of de-hedging, as well as the amounts that were involved in the process, have contributed a significant bump to the price of gold that might not otherwise be manifest today. But let’s allow a picture — courtesy of Thomson/Reuters GMFS — to do the "talking" in this instance. Albeit it might better be titled as "The Net Impact of ProducerDE — Hedging" you get the picture:

Also on the physical metals’ side of the equation, this time for platinum, production difficulties in South Africa have once again made the news with the closure this week of the Angloplats Aquarius Marikana mine in the wake of more labor strife. The platinum market’s one-year high in short positions is seen by Standard Bank (SA) analysts as adding to the possibility of a short-covering rally if news of this type continues. Supply/demand balances in the platinum market are seen as tilting towards an erasure of surplus conditions.

The other type of news that is contributing to robustness in platinum prices is health-related. Two days ago the World Health Organization warned that there is a direct link between diesel engine exhaust and certain types of cancer. It is thought that if more nations begin to impose stricter emissions controls regulation, then the demand for platinum in automobile catalytic converters might grow strongly as well. Platinum loadings are essential in diesel engine-powered cars. Most gas-powered vehicles can rely on palladium loadings even though they also use platinum in the catalytic application.

Moreover, the astounding turn-around in Japanese car output just one year after the devastating Sendai quake is adding to perceptions that the demand side for palladium and platinum remains vibrant. Japan is likely to build over 26 million vehicles before the end of next March and that would be a 16% gain from the previous 12-month period. The palladium market is facing no likely increases in supply-in fact, quite the opposite.

North American Palladium’s CFO Jeff Swinoga noted recently that "In South Africa, there are issues associated with unions, the tax structure they’re putting in place, infrastructure problems and the electricity price increases [power utility] Eskom is putting in place. A lot of South African companies now are in fact talking about curtailing their production in order to save their balance sheets. You’ve got declining palladium production in Russia. There are no new mines that I’m aware of on the horizon."

Analysts at New York-based CPM Group project palladium production going forward to be "relatively flat."

Marketwatch’s Sterling Wong notes that In terms of price forecasts, both TD Bank and BNP Paribas see the price going over $1,000. Today, palladium is at around $615, so there is lots of room for [price] growth."

Indeed, consider the odds for a 62%-magnitude move; is gold (from $1630 to $2650) or palladium (from $615 to $1000) more likely to achieve that feat? And, yes we have even seen $2,100 palladium projections having been made… which would need to equate $5,700 gold for a similar trebling.

"Fedspectations" also continued to make the speculative rounds (see Thursday’s 200-point climb in the Dow and the $1.00 lift in black gold) but a growing number of odds-makers are stepping away from forecasting an outright QE by the Fed and are dialing back their predictions to some sort of extended OT (Operation Twist) or a simple language-based Fed "easing" whereby the 2014 timeframe is reiterated as the target year during which to call it quits on accommodative policies. The Wall Street Journal reports that economists at Credit Suisse are placing 80% odds on the Fed taking "fresh easing measures" next week, with 60% odds of an extension of Operation Twist.

Despite all the current and horrific hard money newsletter depictions of how the Weimar Republic and its hyperinflation levels are "here and now," it turns out that US consumer prices experienced their largest decline in over three years last month. One component of the CPI, the gas index, fell by 6.8% and that’s the largest such decline since late 2008. Core inflation climbed at the 2.3% rate over the past twelve months in the US.

That’s hardly the type of cost-of-living environment where a wheelbarrow-full of greenbacks is required for the purchase of a loaf of bread. Then again, certain subscriptions would be in jeopardy if the latest titles being e-mail blasted to subscribers would mention these figures. Also too taboo to mention would be the fact that American consumer confidence climbed once again last week and reached a high last seen in April. The combination of sharply falling gas prices and record low mortgage rates is easing the burden on US households and lifting their comfort levels.

Now consider inflation (or the lack of high levels of it) in China. A year ago, the country’s CPI was running at 6.5% and it had some folks alarmed. Fast-forward to today: China’s inflation gauge in May showed a reading of 3%. The Credit Suisse estimate for 2013’s CPI temperature in China is 2.3%. The firm’s economists say that this kind of contraction in CPI feels like not only disinflation, but deflation to some of the country’s corporations. To be fair however, the swings that have been known to occur in Chinese inflation readings are nothing short of spectacular. For example, CPI was at 8.7% in February of 2008 only to be followed by negative readings just one year later, for nine straight months through late 2009.

That gets tiring just writing about it.

Meanwhile, growth forecasts for China are being scaled back almost with each passing day. Bloomberg News reports that Credit Suisse Group AG (CSGN) and Deutsche Bank AG reduced forecasts for China’s growth this year as weakness in exports and in investment drag on the world’s second-biggest economy. Credit Suisse cut its estimate to 7.7 percent from 8 percent, while Deutsche Bank lowered its forecast to 7.9 percent from 8.2 percent, according to e-mailed research notes received today. The predictions indicate the weakest growth since 1999 and compare with a 9.2 percent expansion [that occurred] last year.

The debt crisis in the Old World showed signs of further aggravation n Thursday with fresh downgrades of Spain, Cyprus, and now even France, bond yields soaring for Spain and Italy, and continuing difficulties in the regional equity markets. While all eyes are on Germany (and the ECB) as the source of some eventual solution to what ails the EU at the moment, German Chancellor Merkel tried to make it quite clear that her country cannot bear the entire weight of the Herculean task at hand.

The Financial Times reports that Ms. Merkel bluntly stated that "Germany’s resources are not unlimited and Germany’s strength is not infinite." The Chancellor’s forceful restatement of German limitations on any future action to address the debt mess came before next week’s G-20 summit in Mexico. To be continued…

A Thursday afternoon Reuters report indicating that central banks were ready "move" to provide liquidity, if necessary, in the hours following the upcoming Greek elections temporarily lifted equities (the Dow was up 200 points after the rumor then fell back to being up only 130 points), the common currency (the euro jumped to above $1.26 against the dollar), and gold (which went from being up $1.20 to $7.50 in a matter of seconds) and pulled down the US dollar to just under the 82.00 mark on the trade-weighted index.

Marketwatch relays the fact that experts in Washington said on Thursday that Greece could exit the euro zone within weeks or months if the far-left party Syriza — the second largest party in Greece — wins the election Sunday and forms a coalition. Whether a victory by Syriza will be sufficient to seize up the global financial system and lead to some central bank intervention on Monday remains to be seen.

However, analysts at London-based Capital Economics opine that "the central banks which matter most are unlikely to agree to further significant policy stimulus this year unless and until the crisis in the euro-zone deteriorates further."

At this point, we suppose, it all boils down to one’s definition of "further."

In any event, outsized reactions, such as the above, from the currency, commodity, and equity markets are to be expected (in either direction) after the polls close in Greece. There could be (short-lived) euphoria, or there could be (equally short-lived) "tantrums" to be witnessed as markets open for business on Monday morning. The "good news" is, that time is merely hours away, as is the G-20 meeting in Los Cabos, and, as is the Fed meeting on Tuesday and Wednesday.

Get those coffeemakers fired up, and your computer screens freshly Windexed. Such "planetary alignments" do not occur very frequently in the world of money.

Have a nice weekend.

Jon Nadler

Senior Metals Analyst — Kitco Metals

Jon Nadler

Senior Metal Analyst

Kitco Metals Inc.

North America

Disclaimer: The views expressed in this article are those of the author and may not reflect those of Kitco Metals Inc. The author has made every effort to ensure accuracy of information provided; however, neither Kitco Metals Inc. nor the author can guarantee such accuracy. This article is strictly for informational purposes only. It is not a solicitation to make any exchange in precious metal products, commodities, securities or other financial instruments. Kitco Metals Inc. and the author of this article do not accept culpability for losses and/ or damages arising from the use of this publication.

www.kitco.com and www.kitco.cn

Blog: http://www.kitco.com/ind/index.html#nadler