Friday’s last minute "I won’t go home flat just in case" type pop in gold prices netted the yellow metal a $6.40 gain on the day but it fell short of erasing the 1.9% decline that gold suffered on the week.

Friday’s last minute "I won’t go home flat just in case" type pop in gold prices netted the yellow metal a $6.40 gain on the day but it fell short of erasing the 1.9% decline that gold suffered on the week.

Polled market observers had gone into last week’s action convinced that bullion was going to build on the large gains achieved on the previous Friday. Alas, Fed Chairman Bernanke took the bullish wind out of their speculative sails with his poker face flavored (as regards further QE) presentation on Capitol Hill.

The new trading week got off to a relatively strong start overnight as gold prices opened firmer overseas and they briefly retook the $1,600 level shortly after the market opened at 6:00 PM New York time. The bulk of the gains were driven by the perception that the rescue plan for Spain’s banks would be euro-beneficial. As it turned out, at least during the evening hours, the euro climbed to above the $1.26 mark and the US dollar dipped briefly amid similar expectations of some temporary success in addressing the region’s crisis.

The Commitment of Traders Report (COTR) for the week ending Tuesday, May 29, 2012, tallied a notable increase in long gold positions, and a concurrent reduction of short positions. However it should also be expected that a sizeable number of those new long positions have already been stopped out or unwound in the aftermath of Mr. Bernanke`s testimony to the US Congressional Committee on Thursday and in the wake of the resulting aggressive sell-off in gold.

The silver market’s speculative positioning shows that only a modicum of unwinding has taken place among shorts and as such the development still points to a metal whose players have not abandoned their mostly bearish view of it. A somewhat similar lack of conviction is also apparent in platinum; however the ETFs have come back as net buyers into palladium and are showing a distinct preference for it within the PGM space.

While still remaining of the opinion that the "set up is in place of a break under the $1,527 support shelf, finally" Friday night’s EW update advises that "while not expected, a rally above last week’s $1,641 high" could alter the near-term forecast and suggest a more "protracted upswing" was underway. Whether or not an upswing in the share price of Barrick Gold (following the ouster of its last CEO) is in the cards, remains unclear at this point. It is, however, interesting to note that the very vehicle which the miners clamored to launch back in 2004 — the gold ETFs- may be the culprits behind the "performance dysfunction" of some of these stocks.

As MSN Money points out, "The pressure on the [Barrick] share price was also intensified by a growing investor taste for gold-backed exchange traded funds (ETFs). Demand for these financially engineered products has tripled in the past five years. They offer pure leverage to gold prices but without the risk of mining accidents, environmental judgments, cost overruns and asset write-downs."

Here is a classic case of "be careful what you wish for" and of a Frankestein-ian — "It’s Alive!!!!" all rolled into one.

Speaking of market forecasts and of the $1,640 value level in gold, the latest projections on gold from the CPM Group indicate that the firm expects the yellow metal to average… $1,639 per ounce this year. The consultancy said that "precious metals are at a cyclical peak in a secular, long-term bull market." CPM also projected a $30 per ounce average price for silver for the current year.

The research and advisory firm identifies two of the components that are contributing to this "cyclical peak" in bullion prices as being: a) a waning investments demand owing to near-record prices, and b) a tempering of previously overblown anxieties about the system.

CPM notes that "One should realize that a bull market, in any asset, carries with it the seeds of its own ending. Prices ultimately rise to levels that shift supply, demand, and investment demand.

The analytical group at CPM also cautions that "This is an immutable economic law, although one which investors repeatedly ignore, whether it is in gold, copper, bank stocks, real estate, Internet stocks, or so many other assets." CPM said that investors [have] now distanced themselves from "the unbridled, sometimes irrationally overblown, fears of imminent financial system collapse and economic depression that had been driving them to buy enormous amounts of gold and silver regardless of the price, until September 2011 [when prices peaked at $1,920 and change]."

Spot metals dealings in New York this morning opened on the plus side for all components in the complex but gold. The yellow metal was quoted at $1,591 down about $3 while silver climbed 15 cents to $28.68 the ounce. Platinum was up $16 at $1443 and palladium advanced $6 to $619 per ounce. No changes were reported in rhodium at $1,225 the ounce. In the background, the US dollar held firm near 82.25 on the index while the euro retreated to just above $1.25 and overnight gains in Spanish equities and oil were pared after the effects of the Spanish bank bailout news faded a bit.

In general, while the news from Spain did encourage gloomy euro players initially, they are still seen as having greeted it with only tepid sentiment and they appear to now be anxiously focusing on the upcoming Greek elections on the 17th. Certainly, judging by the yield on Spanish bonds (now at 6.38% and up from Friday’s 6.24%) suggests that the market is looking beyond the bank rescue and is beginning to price in a sovereign debt "problem" (we don’t want to jinx this by using the word "default"). Some "vigilantes" have already begun looking even beyond Spain and are pulling Italy into the crosshairs.

And now, let’s move on over to China. As had been suspected, last week’s surprise quarter-point cut in interest rates by the PBOC was indeed a "sweetener" for what was to come in the days ahead; the May list of key economic metrics. The raft of Chinese economic statistics released over the weekend indicates on-going sluggishness in that country’s economy. Line items such as retail sales and fixed-asset investment were down and industrial output remained notably under long-term averages despite a small upward bump in May.

In all, the aggregate metrics still point to China’s worst quarter in three years. If any of the numbers that were made public offered any comfort to the country’s leadership, those would be related to the temperature readings related to inflation. China’s CPI ebbed to 3 percent last month and that was the lowest pace that consumer prices have increased at, in two years’ time.

China watchers concluded that while the economic math contained in the latest statistical harvest points to softness, the need for large-scale, aggressive stimulus by the central bank has not yet become pressing. However, one can remain reasonably sure that the PBOC is not going to take its eyes off of certain areas of the economy that produced dismal readings recently; the manufacturing and services sectors, and consumer sentiment.

Other types of analysts will continue to focus on areas that could offer even more telling clues as to what might be in the cards for the Chinese economy, chief among them, the levels of stockpiles in certain key commodities.

Tsinghua University Business Professor Patrick Chovanec advises that "much more significant is [to be] looking at inventories of metals and raw materials to read where the economy is going. Steel, aluminum, and copper are all in alarming overcapacity."

Also over the weekend, it became apparent that the eurozone is facing a fourth SOS call for rescue funds by one of the region’s member nations. Spanish officials said on Saturday that the country’s troubled banks will require financial aid which it alone cannot provide. Thus, it has been reported that the EU will grant Spain a loan of about $125 billion with which the banks in question could be recapitalized. Certain websites immediately jumped on the Spanish news by declaring that it was the catalyst that will now (okay, by the end of summer, give or take) propel gold to $2K and silver to $60 an ounce.

Spain’s real estate mania of the 90’s has come back to haunt the country’s banks with a vengeance. A decline of more than 30% in home values, unemployment levels above 24 percent and a current list of as many as one million unsold properties have resulted in loan delinquency rates as high as 19% at certain banks. There are no solid estimates of the total size of their aggregate toxic assets. Shortly after he hailed the rescue package by declaring that "Europe has been up to the challenge" Spain’s Prime Minister Rajoy flew off to Poland to watch his country take part in a more important… challenge; a soccer match against Italy.

Of course, the news flows from the Old World will continue to affect the markets not only this week and beyond, but they have also affected them (and the US economy) to quite an extent in the year to date. Wednesday’s release of May US retail sales numbers may corroborate the fact that American consumers may have lost some confidence on the heels of all the bad stories coming out of Europe and that they have spent less as a result of such conditions. Lower car sales levels may be the principal swing factor in what is estimated to be a 0.3% decline in US consumer spending last month.

On Friday we will learn how Mr. & Mrs. US Mall Shopper feels about things economic overall, as reflected by the University of Michigan sentiment survey. Indications are that Europe-centric anxieties could make for a dip in such sentiment. However, there could be one bright spot on offer in the week’s statistics as regards consumers. The sharp fall in crude oil from $110 to under $85 per barrel could spell a decline in US inflation and also give the American consumer a bit of extra cash to spend on things other than topping off the gas tanks of their SUVs. PPI and CPI are both thought to have eased in the past month.

Having read more than our fair share of hard money publications and alarmist "How to Profit From… [insert your favorite doomsday scenario here]" books over the past several years, it would not be hard to be suffering from a severe bout of anxiety over hyperinflation. It — by all accounts- should, right here, right now, be devouring our life savings at a phenomenal clip because of what the Fed did back when the financial crisis hit hard. Go figure that, three years after the Great Recession ended in June of 2009, the principal threat to the US economy (and your wealth) is actually… deflation.

A brief preview of that paradigm was on offer during the summer of 2008 and everyone knows it is a situation far from pleasant. Currently, there are at least five watch items on the list which continues to point to the resurgence of deflation (and not the emergence of the Weimar Republic on the banks of the Potomac). They are: the price of black gold, the price of other commodities, the output gap in the US economy, the T-bond market, and the shrinking number of federal, state, and local workers in government. The Atlanta Fed places the odds of deflation in the US at 14% over the next five years. This, while a plethora of publications place the odds of 50% per month inflation (the criterion for the "hyper" label) at 101% like… yesterday or the day before.

Then again, there are other myths and misconceptions being bandied about in this US election year, in ample supply. One of them regards the idea that supply-side economics is worth pursuing as it results in more jobs, and happier citizens in all walks of life. Not quite. See the table. One of the biggest tenets of the supply-siders is that tax cuts result in economic miracles. MarketWatch analyst Howard Gold begs to differ. He cites a growing body of economists who would take Mr. Laffer’s napkin containing a certain famous curve and who would employ said napkin for its originally intended use.

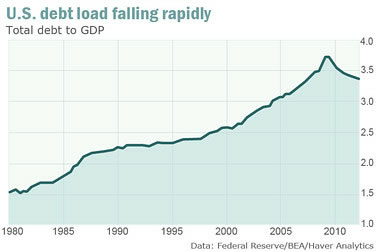

The other "tall tale" being recounted to death in the aforementioned cottage industry of scaremongering that has sprung up in the wake of the 2008 crisis is the one about America’s debt load. You know: America’s debt is unsustainable; it will kill the dollar, your money, the country, democracy, etc. Well, MarketWatch’s Rex Nutting blows a gaping hole into that assertion by referring to this little chart — for starters:

Bet you were not aware (from your habitual readings) that America’s debt burden is gradually being reduced. The process is called de-leveraging. It is still underway.

It seems to be working. Mr. Nutting notes that "since the recession ended in June 2009, total US debt has risen at the slowest pace since they began keeping records in the early 1950s."

The ratio of total US debt to US GDP has fallen from 3.73 times GDP to 3.36 times GDP at last count. In the 33 months that have elapsed total domestic US debt has climbed by only $702 billion, or 1.4%. Now consider 2005-2007 when America’s total debt ballooned by over $10 trillion or 28%. The above are but two examples of "sacrosanct" arguments that certain factions in this market rely upon and sell you as "Gospel truth" when trying to "sway" your investment decisions into an extreme direction.

As we have said before: "Caveat Lector" applies once again. Every story — including ones thought to be bullet-proof — has another side.

Until Wednesday,

Jon Nadler

Senior Metals Analyst — Kitco Metals

Jon Nadler

Senior Metal Analyst

Kitco Metals Inc.

North America

Disclaimer: The views expressed in this article are those of the author and may not reflect those of Kitco Metals Inc. The author has made every effort to ensure accuracy of information provided; however, neither Kitco Metals Inc. nor the author can guarantee such accuracy. This article is strictly for informational purposes only. It is not a solicitation to make any exchange in precious metal products, commodities, securities or other financial instruments. Kitco Metals Inc. and the author of this article do not accept culpability for losses and/ or damages arising from the use of this publication.

www.kitco.com and www.kitco.cn

Blog: http://www.kitco.com/ind/index.html#nadler